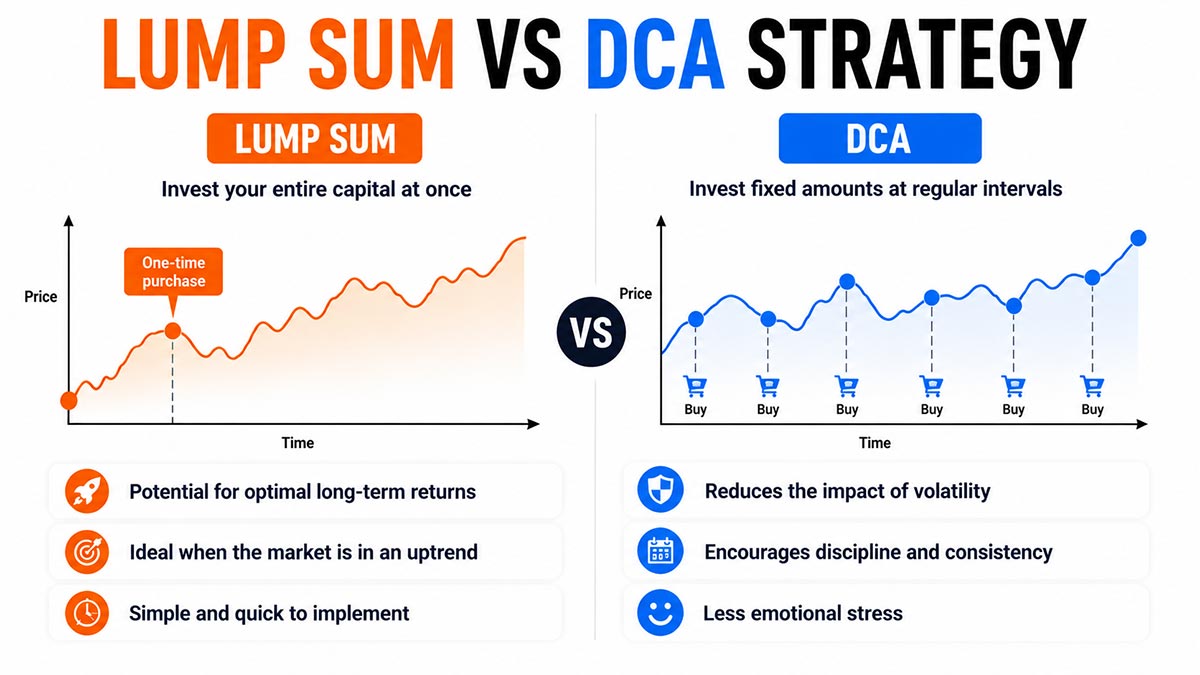

Lump-sumLump-sumInvesting all available capital at once rather than spreading it out. Mathematically better on average historically on Bitcoin, but psychologically harder to bear.See in the lexicon → means investing an amount in one go, at a given instant. DCADCA (Dollar Cost Averaging)Buying a small fixed amount at regular intervals (for example 100 EUR a week), regardless of price. Smooths the average purchase cost and neutralises timing bias.See in the lexicon → means spreading it over several months or years. The "lump-sum or DCA" question arises as soon as one has a sizeable amount to allocate (inheritance, bonus, property sale, years of accumulated savings) and the binary entry decision weighs on the return.

A 2012 Vanguard study found that on the S&P 500, lump-sum beats DCA in about 66 % of 10-year cases : entering early captures the market's upward drift. But this result does not transpose mechanically to Bitcoin, whose volatility (~250 %) is ten times that of the S&P 500. On Bitcoin, the timing risk becomes asymmetric : entering at a cycle top can impose 3 years of drawdownDrawdownDecline from a previous peak. Bitcoin has gone through several drawdowns of more than 75 percent in its history. To factor into your psychological planning.See in the lexicon → before reverting to the mean.

This article lays out the mechanics of both approaches, the Vanguard study and its limits, a retroactive Bitcoin simulation 2019-2026 at several entry points (2017 top, 2018 bottom, 2021 top, 2022 bottom), a 4-criterion decision tree (amount, horizon, conviction on the cycle, psychological tolerance), and the hybrid variant (partial lump-sum plus DCA spread over 12 months).

Lump-sum and DCA: precise definitions

Before comparing, let's fix vocabulary. Both strategies answer the same question ("how to deploy a given capital into Bitcoin") but with opposite temporal parameters.

- Lump-sumLump-sumInvesting all available capital at once rather than spreading it out. Mathematically better on average historically on Bitcoin, but psychologically harder to bear.See in the lexicon → (sometimes "one-shot") designates a complete and immediate investment of a given capital at a chosen time T. Example: Pierre receives 50,000 EUR on 15 May 2026 and buys 50,000 EUR of BTC on 20 May 2026, in one or two orders executed within the week. The capital is fully exposed to the market from the start. The buy timing fully conditions the result.

- DCADCA (Dollar Cost Averaging)Buying a small fixed amount at regular intervals (for example 100 EUR a week), regardless of price. Smooths the average purchase cost and neutralises timing bias.See in the lexicon → (Dollar Cost Averaging, detailed in the Bitcoin DCA method article) here means a capital deployment DCA: fragmenting the initial capital into N fixed-size buys over a short period (typically 6 to 24 months). Example: Pierre buys 2,083 EUR of BTC every week for 24 weeks, 50,000 EUR total. This deployment DCA differs from permanent recurring DCA (Lucas stacking 100 CHF/week indefinitely). Here the total capital is finite and time-bounded.

Three variants for Pierre to know.

- Short DCA (6 months): 50,000 / 26 = 1,923 EUR per week for 6 months. Advantage: capital fully deployed in less than a year, maximum exposure to a possible rally. Drawback: if you enter at cycle top, smoothing is insufficient.

- Medium DCA (12 months): 2,083 EUR per week for 12 months. Classic compromise, recommended by most Bitcoin advisers for large amounts. Properly smooths half a cycle.

- Long DCA (24 months): 1,041 EUR per week for 24 months. Advantage: covers almost a full Bitcoin cycle (cycles last ~3.5 to 4 years). Drawback: leaves a large part of the capital in unremunerated cash for 2 years, and inflation erodes real value.

For the rigorous comparison in this article, the convention is weekly 12-month DCA. This is the academic standard and the most commonly practised in reality.

Permanent recurring DCA (Lucas stacking 100 CHF/week endlessly) is not compared here as it answers a different question: not "how to deploy existing 50,000 EUR" but "how to invest a monthly savings flow". For recurring DCA, see the dedicated Bitcoin DCA method article.

The 2012 Vanguard study: on stocks, lump-sum wins 66 % of the time

The academic reference study on the question is Dollar-Cost Averaging Just Means Taking Risk Later, published by Vanguard Research in July 2012, authored by Anatoly Shtekhman, Christos Tasopoulos and Brian Wimmer. It is the most complete and most cited empirical work on the subject.

Methodology. Vanguard compared lump-sumLump-sumInvesting all available capital at once rather than spreading it out. Mathematically better on average historically on Bitcoin, but psychologically harder to bear.See in the lexicon → vs 12-month DCADCA (Dollar Cost Averaging)Buying a small fixed amount at regular intervals (for example 100 EUR a week), regardless of price. Smooths the average purchase cost and neutralises timing bias.See in the lexicon → on three historical stock markets: United States (S&P 500 or equivalent, 1926-2011), United Kingdom (FTSE All-Share, 1976-2011), Australia (All Ordinaries, 1984-2011). For each market, the study split history into thousands of 10-year rolling windows and compared, for each window, the final result between both strategies, assuming a 60/40 stocks/bonds mixed portfolio (the standard retiree mix). Total: over 1,000 independent simulations per market.

Main result. Lump-sum produced a final return higher than DCA in approximately 66 % of observed cases, across all three markets and all considered windows. United States: 67 %. United Kingdom: 68 %. Australia: 67 %. Consistent across jurisdictions and periods. The average return surplus of lump-sum over DCA is +2.3 % over a 10-year horizon (~+0.23 % per year), with a significant standard deviation.

Intuitive explanation. Stock markets have a long-term upward tendency (the "upward bias"). On the S&P 500, the real annualised return is ~7 % since 1926. So statistically, the market goes up 2/3 of the time over 10-year windows. Lump-sum maximises exposure to this upward bias from the start. DCA postpones exposure, leaving under-remunerated cash for 12 months during which the market (often) keeps rising. This opportunity cost mathematically explains the 66 % lump-sum wins.

Important nuances the study provides.

- In the remaining 34 % of cases (lump-sum loses), the magnitude of lump-sum loss is on average larger than the magnitude of gain in the 66 % of wins. Classic risk asymmetry: when it goes bad, it goes really bad.

- DCA reduces the volatility of the final result, not the expected return. On the 60/40 mix, the standard deviation of final returns is ~25 % lower in DCA. That is the psychological argument: sleep peacefully rather than maximise expectation.

- On bear or prolonged stagnation markets (Japan 1989-2009 for example, not directly covered by the Vanguard study but documented elsewhere), DCA clearly beats lump-sum. The 66/34 result depends on the average upward bias; it collapses in durably bearish contexts.

Academic conclusion. On mature stock markets, lump-sum is statistically superior 2/3 of the time. But the gap is modest (~+2.3 % over 10 years), at the cost of higher result volatility. Vanguard recommends lump-sum provided the investor is psychologically able to absorb an immediate 30 % drawdownDrawdownDecline from a previous peak. Bitcoin has gone through several drawdowns of more than 75 percent in its history. To factor into your psychological planning.See in the lexicon → without panicking. Otherwise, DCA for mental tranquility, assuming the average expectation loss.

Why Bitcoin differs from the S&P 500

The Vanguard 66/34 result does not transfer mechanically to Bitcoin. Three structural differences upset the equation.

1. Volatility 4 to 5 times higher.

- S&P 500 annualised volatility: ~15-20 % (depending on period, more stable since 1990).

- Bitcoin annualised volatility: ~70-90 % (over 2014-2026, gradually declining from 100 % to 60 % with maturation, but still several times higher than stocks).

- Direct consequence: Bitcoin drawdowns are brutal. The S&P 500 had two -50 % drawdowns in a century (1929-1932 and 2008-2009). Bitcoin had five -80 % drawdowns in 15 years (2011, 2014, 2018, 2022, and a partial -75 % in 2025). A mistimed lump-sumLump-sumInvesting all available capital at once rather than spreading it out. Mathematically better on average historically on Bitcoin, but psychologically harder to bear.See in the lexicon → on Bitcoin potentially means -80 % in months; impossible on S&P 500 outside systemic crisis.

- DCADCA (Dollar Cost Averaging)Buying a small fixed amount at regular intervals (for example 100 EUR a week), regardless of price. Smooths the average purchase cost and neutralises timing bias.See in the lexicon →, which reduces result variance, is therefore mathematically more useful on Bitcoin than on stocks. The psychological protection it offers is worth more when potential drawdowns are -80 % than when they are -30 %.

2. Pronounced 4-year cycles (halvingHalvingScheduled event every 210,000 blocks (roughly every 4 years) that cuts the miner reward in half. This mechanism makes Bitcoin issuance decline towards the total cap of 21 million.See in the lexicon →).

- Bitcoin shows a ~4-year cyclical pattern, mechanically linked to halvings (issuance halving every 210,000 blocks, ~4 years). Observed cycles: bull 2010-2011, bear 2012, bull 2013, bear 2014-2015, bull 2016-2017, bear 2018, bull 2020-2021, bear 2022, bull 2023-2025, likely ongoing bear 2026.

- Stocks have no such marked and predictable cycle. Stock cycles exist (~10 years) but are less synchronised and much less ample (-20 % to -50 % drawdowns, not -80 %).

- Consequence: entry timing has a much more determining weight on Bitcoin than on S&P 500. Buying at the 2017 cycle top (Dec 2017 at 16k EUR) or bottom (Dec 2018 at 3.7k EUR) changes outcome by a factor 4. On S&P 500, the gap between top and bottom of a 10-year cycle is typically a factor 1.5 to 2.

- DCA attenuates this catastrophic timing risk by smoothing over a partial cycle.

3. Adoption phase, not maturity phase.

- Bitcoin is 17 years old in 2026. The S&P 500 has existed since 1957 (with predecessors since 1923, 100 years). The NYSE since 1817. US stocks are in maturity phase, with established valuation models (DCF, PE ratios, dividends).

- Bitcoin is still in price discovery, with an increasing adoption logic (institutions, States, spot ETFs validated in 2024, MiCAMiCA (Markets in Crypto-Assets)European regulation 2023/1114 that frames crypto services across the EU since 2024. Creates the CASP status.See in the lexicon → Europe in 2025-2026). Price fundamentals (21 million21 millionMaximum number of bitcoins that will ever exist, hard-coded in the protocol. This programmed scarcity is a founding feature. The last sat will be mined around the year 2140.See in the lexicon → capped supply, growing demand, S2FS2F (stock-to-flow)Valuation model comparing existing stock with annual production, popularised by PlanB. Appealing to illustrate Bitcoin's growing scarcity, but empirically contested.See in the lexicon → curves, monetisation models) trend long term upward, but with huge variance over short windows.

- Consequence: Bitcoin's long-term expectation remains bullish (at least per dominant models), like S&P 500 expectation. But short-term variance is much greater, favouring DCA smoothing for large portfolios.

Summary. On Bitcoin, the Vanguard principle still holds (on average, lump-sum better captures upward expectation). But the lump-sum advantage is more modest in relative terms due to brutal cycles, and the cost of bad timing is much more catastrophic. The balance leans more toward DCA than on stocks. This is what the retroactive simulation in the next section confirms with numbers.

Retroactive simulation: 20,000 EUR at 4 key points 2017-2022

To make the comparison concrete, let's simulate a 20,000 EUR investment at 4 very different historical entry points, in lump-sumLump-sumInvesting all available capital at once rather than spreading it out. Mathematically better on average historically on Bitcoin, but psychologically harder to bear.See in the lexicon → vs weekly 12-month DCADCA (Dollar Cost Averaging)Buying a small fixed amount at regular intervals (for example 100 EUR a week), regardless of price. Smooths the average purchase cost and neutralises timing bias.See in the lexicon →. Final valuation at 2026-05 (price ~90,000 EUR/BTC). DCA average prices are calculated from weekly Bitstamp euro prices over the 52 weeks following the entry point.

| Entry point | Cycle context | Lump-sum BTC acquired | 12-month DCA BTC acquired | Lump-sum May 2026 | DCA May 2026 | Winner |

|---|---|---|---|---|---|---|

| Nov 2017 (16,000 EUR/BTC) | 2017 cycle top | 1.25 BTC | ~2.55 BTC (DCA avg ~7,850 EUR) | 112,500 EUR (+462 %) | 229,500 EUR (+1,048 %) | DCA (+2x) |

| Dec 2018 (3,700 EUR/BTC) | 2018 bear bottom | 5.40 BTC | ~3.06 BTC (DCA avg ~6,540 EUR) | 486,000 EUR (+2,330 %) | 275,400 EUR (+1,277 %) | Lump-sum (+1.77x) |

| Nov 2021 (58,000 EUR/BTC) | 2021 cycle top | 0.345 BTC | ~0.53 BTC (DCA avg ~38,000 EUR) | 31,050 EUR (+55 %) | 47,700 EUR (+138 %) | DCA (+1.54x) |

| Nov 2022 (16,000 EUR/BTC) | 2022 bear bottom | 1.25 BTC | ~0.83 BTC (DCA avg ~24,100 EUR) | 112,500 EUR (+462 %) | 74,700 EUR (+274 %) | Lump-sum (+1.5x) |

Reading the table. Lump-sum wins at both bottom points (2018 and 2022), DCA wins at both top points (2017 and 2021). Result is binary in lump-sum: brilliant at bottom, catastrophic at top. DCA is always intermediate: never the best possible outcome, but never the worst either.

Three crucial observations.

- Lump-sum psychological asymmetry. Buying 1.25 BTC at 16k EUR in November 2017 and seeing the portfolio drop to 4,600 EUR in December 2018 (-71 %) is psychologically unbearable for most retail investors. Many would have panic-sold at the trough. The final +462 % result assumes one held for 8.5 years despite crypto winter. This is a major psychological test. The November 2017 DCAer saw their portfolio progress more steadily and never had to suffer maximum drawdownDrawdownDecline from a previous peak. Bitcoin has gone through several drawdowns of more than 75 percent in its history. To factor into your psychological planning.See in the lexicon → on 100 % of capital.

- The 4-factor gap between the 4 scenarios. The best lump-sum outcome (486k EUR at 2018 bottom) is 15x the worst (31k EUR at 2021 top). DCA reduces this gap to a factor ~5 (275k vs 47k). DCA variance is markedly lower: direct consequence of temporal smoothing.

- Average over 4 scenarios. Lump-sum total: 742k EUR (average return +827 % per scenario). DCA total: 627k EUR (average return +684 % per scenario). Lump-sum wins ~18 % in cumulative value. Consistent with Vanguard (lump-sum favourite in expectation) but the gap is narrower than on stocks (~10 % over 8.5 years), because losses at top heavily degrade the lump-sum average.

Simulation sensitivity. Results depend on the assumed final price (90k EUR in May 2026). With a more optimistic future price (150k EUR), the 2018-bottom lump-sum does +3,900 % and crushes everything. With a pessimistic price (50k EUR), the 2017-top lump-sum does -69 % and remains a loser against DCA. The qualitative conclusion (binary lump-sum, intermediate DCA) does not change.

4-criteria decision tree + 50/50 hybrid variant

To decide between lump-sumLump-sumInvesting all available capital at once rather than spreading it out. Mathematically better on average historically on Bitcoin, but psychologically harder to bear.See in the lexicon → and DCADCA (Dollar Cost Averaging)Buying a small fixed amount at regular intervals (for example 100 EUR a week), regardless of price. Smooths the average purchase cost and neutralises timing bias.See in the lexicon →, here is a 4-criteria practical decision tree, calibrated on Bitcoin adviser experience and academic literature.

Criterion 1: amount relative to net worth.

- Small amount (< 10 % of net worth): lump-sum acceptable. Theoretical maximum drawdownDrawdownDecline from a previous peak. Bitcoin has gone through several drawdowns of more than 75 percent in its history. To factor into your psychological planning.See in the lexicon → (-80 % on this amount) remains absorbable without destabilising overall net worth. Pierre with 50k EUR on 800k net worth can consider lump-sum.

- Large amount (10-25 % of net worth): DCA strongly recommended. Psychological and financial protection of smoothing becomes crucial. A -80 % on 20 % of net worth = -16 % of total net worth, painful but survivable. In lump-sum, it's in one go; in DCA, it's spread out.

- Very large amount (> 25 % of net worth): DCA mandatory, ideally over 24 months or more. Beyond 25 % exposure to such a volatile asset, it's a question of asset risk management, not just timing.

Criterion 2: investment horizon.

- Short horizon (< 3 years): trick question. Bitcoin is not a short-term asset. Over 3 years, you can land on any cycle segment, including a -70 % bear. Lump-sum or DCA, secondary question: maybe Bitcoin is not suitable at all.

- Medium horizon (3-7 years): DCA recommended. 3-7 years covers 1-2 cycles; DCA effectively smooths initial timing risk.

- Long horizon (> 7 years, ideal 10+): lump-sum becomes competitive again. Over 10+ years with 2-3 complete cycles, the Bitcoin upward bias dominates and initial timing fades into noise. This is the scenario where Vanguard approaches: on 10-year windows, lump-sum wins 66 % of the time, even on Bitcoin.

Criterion 3: conviction about current cycle.

- Conviction "we are in a deep bear marketBear market, bull marketProlonged falling market (bear) or rising market (bull). Bitcoin cycles have historically alternated between the two around halvings, with 70 to 85 percent drops in bear markets.See in the lexicon →": lump-sum justified. Buying at 2018 or 2022 cycle bottom was the most profitable decision historically. But warning: bottoms are rarely identified in real time.

- Conviction "we are mid-cycle": classic 12-month DCA. The default case, least informational.

- Conviction "we are at euphoric bull marketBear market, bull marketProlonged falling market (bear) or rising market (bull). Bitcoin cycles have historically alternated between the two around halvings, with 70 to 85 percent drops in bear markets.See in the lexicon → top": long DCA (18-24 months) or wait-and-see. Lump-sum at cycle top is documented as the worst Bitcoin decision (see retroactive simulation section 5, Nov 2017 and Nov 2021).

- Disclaimer. Identifying in real time where we are in the cycle is notoriously difficult. Criterion 3 must be used with caution and corrected by the others.

Criterion 4: psychological drawdown tolerance.

- Experienced investor having already absorbed a -50 % without panicking: lump-sum possible (respecting criteria 1 and 2).

- First large Bitcoin investment: DCA strongly recommended. The first real drop (-30 % or more) is traumatic if unprepared. DCA fragments the psychological impact and teaches to live with volatility.

- Investor known for panic-selling: DCA absolutely, ideally long (24 months). And even consider reducing the global target allocation.

The hybrid variant: partial lump-sum + DCA.

Pragmatic compromise observed among many Bitcoiners 2024-2026: invest 50 % of capital in lump-sum from day one, and 50 % in weekly DCA over 12 months. Pierre would thus deploy 25,000 EUR all at once on 20 May 2026, then 25,000 / 52 = 480 EUR per week for 52 weeks.

Mathematical advantages of this variant:

- Immediate capture of 50 % exposure to upward bias (the Vanguard lump-sum argument).

- Smoothing of 50 % of capital over 12 months (protection against bad timing).

- On the 4-entry-point retroactive simulation (section 5), the hybrid variant averages ~705k EUR on 80k invested, between pure lump-sum (742k) and pure DCA (627k). But with significantly lower variance than pure lump-sum.

- Psychological benefit: immediate participation in any rally, not paralysed by "I should have invested everything".

This is the strategy often recommended by pragmatic Bitcoin advisers for inheritances, bonuses and property sales above 30,000 EUR. Application to Pierre: 25,000 EUR on 20 May 2026 (bought outright at 92k EUR/BTC = 0.272 BTC), then weekly DCA 480 EUR over 12 months. If Bitcoin rises, the lump-sum half captures; if Bitcoin falls, the DCA buys cheaper.

Specific traps of each strategy

Beyond the mathematical choice, each strategy has its documented behavioural traps. Knowing them avoids half the mistakes.

Lump-sumLump-sumInvesting all available capital at once rather than spreading it out. Mathematically better on average historically on Bitcoin, but psychologically harder to bear.See in the lexicon → traps.

- Top buying FOMOFOMO (Fear Of Missing Out)Fear of missing the rally, which pushes people to buy at the worst moment, near the tops. DCA is the classic antidote.See in the lexicon →. "The price keeps rising weekly, I buy everything now before it rises more." Classic pattern observed in November 2017 and November 2021. Lump-sum triggered by euphoria produces the worst documented outcomes (-80 % over following 12 months). Test: if you feel like lump-summing after a +30 % monthly rise, it's probably the worst period.

- Analytical paralysis. "I'll wait for a 20 % correction to enter, it'll come soon." Pattern observed in Bitcoiners who missed the entire 2020-2021 bull waiting for a dip that never came in time. Paralysis can last 18 months during which the price does +200 %. Test: if you've been procrastinating for over 3 months, that's the sign to force a decision (hybrid DCADCA (Dollar Cost Averaging)Buying a small fixed amount at regular intervals (for example 100 EUR a week), regardless of price. Smooths the average purchase cost and neutralises timing bias.See in the lexicon → at minimum).

- Anchoring effect on purchase price. "I bought at 100k, I only sell at 100k+." Anchoring to purchase price drives bad sale decisions. If price drops to 60k and long-term thesis collapses, anchoring prevents cutting the loss. DCA mitigates this bias by diluting purchase price across several levels.

- DrawdownDrawdownDecline from a previous peak. Bitcoin has gone through several drawdowns of more than 75 percent in its history. To factor into your psychological planning.See in the lexicon → over-reaction. Lump-sum exposing 100 % of capital to timing, immediate drawdown is psychologically maximal. Many panic-sell at cycle trough (2018 capitulationCapitulationFinal phase of a bear market where the last sellers give in to panic, often on record volume. Frequently marks the cycle bottom.See in the lexicon →, 2022 capitulation). Statistically the most destructive decision a BitcoinerBitcoinerPerson interested in Bitcoin, who holds some and adheres more or less to its values (individual sovereignty, sound money, decentralisation).See in the lexicon → can make. DCA mechanically mitigates by exposing less capital at drawdown moment.

DCA traps.

- Regret of not lump-summing in a manifest bull marketBear market, bull marketProlonged falling market (bear) or rising market (bull). Bitcoin cycles have historically alternated between the two around halvings, with 70 to 85 percent drops in bear markets.See in the lexicon →. If DCA starts in bear and market rebounds immediately, the DCAer watches the price rise and buys higher each week, when lump-sum would have caught everything at lows. That's the statistical opportunity cost of DCA (the 66 % where lump-sum wins). Psychological test: can you mechanically hold DCA even when you see you should have lump-summed?

- Continuing DCA in euphoric bull without dynamic adjustment. If the market shifts from bear to bull during DCA, some keep buying mechanically at increasing prices, instead of adjusting (slowing DCA or stopping). The dynamic DCA variant (reduce buys when price exceeds +50 % over 200-day MA, increase when it drops) is more performant in theory but requires discipline.

- Under-investing by disguising DCA. A 200 EUR/month DCA on a 500,000 EUR net worth (0.48 % annual Bitcoin exposure) is ridiculously low. The DCAer has the illusion of having "taken position" while actual exposure remains insignificant. Test: does your DCA reach at least 1 % of net worth per year? Otherwise, increase frequency or amount.

- Abandoning DCA in bear marketBear market, bull marketProlonged falling market (bear) or rising market (bull). Bitcoin cycles have historically alternated between the two around halvings, with 70 to 85 percent drops in bear markets.See in the lexicon →. When price drops -50 % and era psychology is negative (2022 bear, potential 2026 bear), many stop DCA "until things stabilise". This is exactly the opposite of what to do: it's in bear that DCA accumulates most BTC for a given amount. Stopping in bear neutralises DCA's main mathematical benefit.

Trap common to both: never starting. The best strategy is the executed one. An imperfect lump-sum at month M+1 beats an optimal DCA never launched by month M+12. If Pierre dithers 6 months between lump-sum and DCA, he'll have stayed in cash 6 months during which Bitcoin may have done +30 %. Decide and execute within the week. The perfect decision is the enemy of the good decision.

Disclaimer

Educational and informational content only: not investment, tax or legal advice. Bitcoin carries significant risks, including high volatility and the possible loss of invested capital. Each reader remains responsible for their decisions; when in doubt, consult a qualified professional in your jurisdiction.

Going further

The lump-sumLump-sumInvesting all available capital at once rather than spreading it out. Mathematically better on average historically on Bitcoin, but psychologically harder to bear.See in the lexicon → vs DCADCA (Dollar Cost Averaging)Buying a small fixed amount at regular intervals (for example 100 EUR a week), regardless of price. Smooths the average purchase cost and neutralises timing bias.See in the lexicon → decision is one brick of the Invest topic. To explore complementary dimensions:

- Invest Bitcoin guide: overview of strategies, asset allocation, global psychology.

- Bitcoin DCA method: to configure a permanent recurring DCA, the 5 dominant 2026 services, optimal frequency.

- Bitcoin spot ETF: alternative to direct DCA via ETF, different tax treatment, upcoming.

- Halving and Bitcoin cycles: understand the 4 years that make timing critical, upcoming.

- Volatility psychology: why holding a -80 % drawdownDrawdownDecline from a previous peak. Bitcoin has gone through several drawdowns of more than 75 percent in its history. To factor into your psychological planning.See in the lexicon → is the hardest, upcoming.

For the buy and store context:

- Buy Bitcoin guide: choose between exchangeExchangeService that lets you buy, sell and swap cryptocurrencies against fiat money. Examples : Kraken, Coinbase, Bitstamp, Bitvavo. Most are custodial.See in the lexicon → and DCA service to concretely execute lump-sum or fragmented buys.

- Store Bitcoin guide: self-custodySelf-custodyModel in which you hold your own private keys. Your bitcoins depend on no third party. This is Bitcoin's founding promise.See in the lexicon →, hardware wallets, seed phraseSeed phraseSequence of 12 or 24 words (usually in English) that encodes your master key. Universal wallet backup : with these words, you can restore your funds on any compatible software.See in the lexicon → to secure deployed capital.

Capital deployment tax (declarable lump-sum inheritance, long-term capital gains, registries) will be covered in the Fiscalité topic (sprint 6 upcoming).